Special to the Philanthropy Journal

Special to the Philanthropy Journal

By Katrina Pipasts, Northern Trust CSPG

For a nonprofit, “Cash is (often) King”: A donor receives a charitable deduction for an outright cash gift and the nonprofit can immediately put it to work to fund a building, a program or a project. However, a donor’s long-term objectives to support a nonprofit might be better accomplished in structuring a deferred gift, such as a charitable gift annuity or a charitable remainder trust.

Each of these structures permits the sale of appreciated assets without immediate taxation (by deferring most and possibly avoiding some capital gains tax), lowering the cost of diversification and creating cash flow. Moreover, a lifetime gift reduces estate taxes as effectively as a bequest, but has the added benefit of providing gift recognition during the donor’s lifetime.

![]()

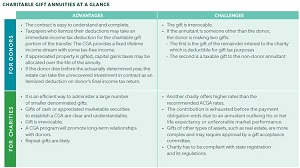

What is a Charitable Gift Annuity (CGA)?

A charitable gift annuity is a contractual agreement between one or two donors and a charity. The donor(s) transfer assets as a gift to the charity and in return, the charity is obligated to pay a fixed annuity to one or two annuitants (recipients of the annuity), for the lifetime of the annuitant(s).

Best Practices for Charitable Gift Annuities

- Establish guidelines for gift minimums, such as $10,000 or higher for a CGA and approve subsequent gift annuities by a repeat donor at a lower minimum such as $5,000.

- Establish a minimum age for immediate charitable gift annuitants – the most common being between 60 and 65 and the average hovering at 70. If the annuity is deferred, it is recommended the minimum age of the annuitant at the time payments begin be the same as the minimum age of an annuitant of an immediate gift annuity.

- The Philanthropy Protection Act of 1995 requires a disclosure statement must be received by the donor in advance of signing the contract to establish a charitable gift annuity. Some states require the inclusion of specific language in the disclosure statement or in the agreement. The American Council on Gift Annuities recommends the charity have the donor acknowledge in writing they have received the applicable disclosure statement.

Click to Enlarge

What is a Charitable Reminder Trust (CRT)?

A charitable remainder trust is an irrevocable trust that generates a potential income stream for the donor, or other beneficiaries, with the remainder of the donated assets going to a charity or charities.

Types of Charitable Reminder Trusts

- The charitable remainder annuity trust (CRAT) is a fixed payment trust. The amount to be paid to the income beneficiary is determined when the trust is first established. The payout percentage is applied to the value of the funding assets to determine the specific fixed payment amount.

- The standard unitrust is a variable payment charitable remainder trust. The unitrust revalues all assets annually. The fixed payout rate is applied to the value of the assets to determine the variable payment amount.

- The net income trust (NICRUT) is a charitable remainder trust that pays out the lesser of the unitrust amount or net income earned by the trust.

- The net income with makeup (NIMCRUT) is a refinement of the net income trust, which allows the unpaid unitrust amount to be paid in any later year when the net income is greater than the unitrust amount.

- The flip trust (FLIPCRUT) is a hybrid of the net income trust and the standard unitrust. These are typically used when the CRT is funded with an illiquid asset with insufficient cash flow.

Because the rules governing the creation and administration of CRTs are complex, the Internal Revenue Service has provided specimen trust agreements for the creation of such trusts.

Mandatory Requirements for Charitable Reminder Trusts

- Required minimum payout is 5%

- Ceiling on the payout rate is 50%

- Projected remainder interest must be at least 10%

- Probability that a CRAT will be exhausted prior to the end of the term is less than 5%

Best Practices for Charitable Reminder Trusts

- Align the appropriate charitable remainder trust vehicle with the unique goals and circumstances of the donor

- Assess the suitability of the asset to fund the trust

- Use specimen trust agreements provided by IRS

Click to Enlarge

What’s Best for Your Donors?

For many donors, the most appropriate philanthropic solution will be determined by consultation with their legal counsel and tax advisors. For some, an outright gift will remain the vehicle of choice. For others, the flexibility of a charitable gift annuity or a charitable remainder trust will fulfill not only their personal financial planning goals, but their charitable intent in supporting a nonprofit for its continued success.

Katrina M. Pipasts is the National Director of Planned Giving Services in the Foundation & Institutional Advisors practice at Northern Trust. She is responsible for the gift administration and investment strategy implementation for charitable gift annuity funds and charitable remainder trusts for institutional clients. She works with a variety of nonprofits to develop and implement best practices for successful planned giving programs.